Equipment leasing adopts the leasing model of replacing funds with leased assets. Lessee acquires the right to use the equipment for operations and manufacturing through leasing without paying a significant amount of cash in advance, only monthly payments during the lease term. Assets that are rented under leases include machine tools, manufacturing equipment, business machines, medical devices, raw materials, etc. Equipment leasing allows SMEs to acquire required equipment and machines without having trouble getting loans from financial institutions because of credit investigation. Lessees can also enjoy advantages like asset accelerated depreciation and lease payments deduction from taxes under tax and accounting relevant regulations.

| Advantages of Equipment Leasing |

No need to pay with large amounts of cash in one time gives you flexibility in

financial planning. |

Companies can add/purchase equipment per plan without being restricted by

loan amount granted by financial institutions. |

Easy control and planning during the duration of the lease which accelerates

change of new models. |

Lease payments of operating lease are expenses and fully tax deductible. |

Capital lease allows the company to claim accelerated depreciation of the

equipment under tax and accounting regulations. |

Partner with niche vendors to reduce the impact of economic downturn. |

|

| |

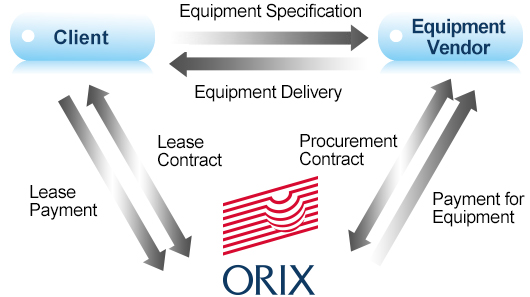

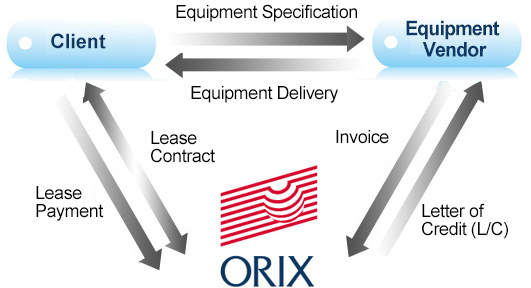

Equipment Leasing Structure

| Domestic Equipment Sourcing |

|

|

| |

| Overseas Equipment Sourcing |

|

|

| |

Leasing Model Comparison

| Leasing option |

Operating Lease |

Capital Lease |

| Asset ownership |

Lessor (ORIX) |

Ownership of the asset will be transferred to the lessee at the end of the lease term. |

| Depreciation claimed by |

Lessor |

Lessee (listed as leased asset) |

| Invoice title |

Rental (full amount claimed) |

Lease payments (principal) and interests |

| Accounting |

Rental/Cash |

*Lease payments should be made for leased asset.

*Itemize based on the invoice when making payments: Rent payable/accrued interest/ Cash

*Monthly payment and interest are calculated by interest rate and are amortized over the lease term (various by month).

*Leased asset turned to fixed asset at the end of the lease term. |

| Pros and cons |

*Not listed as leased asset and liability on financial statement

*No need to do asset cost management. Effectively reduce management cost

*Regular payment, easy for compiling budget

*Tax savings

*No need to pay insurance expense |

Financial statements, asset management and budget compilation induce more difficulties for accounting staff while increasing costs. |

| At the end of the lease term |

*Retrieved by lessor

*Lease renewal |

Leased asset turned to fixed asset. Ownership transferred to lessee at the end of the lease term. |